If you don’t know your numbers, you don’t know your business. It’s that simple. Calculating your production costs comes down to summing up your direct materials, direct labour, and manufacturing overheads. Getting this formula right is the bedrock of a profitable company, shaping everything from your pricing strategy to your final bottom line.

What Are Production Costs and Why They Matter

Before you start wrestling with spreadsheets, let's get clear on what you’re actually counting. Production costs cover every single expense a business racks up while making a product or delivering a service. Think of it as the total price tag for bringing one unit of whatever you sell into existence.

For any UK business, whether you're a local furniture maker in Bristol or a software firm in Manchester, understanding these figures is far more than an accounting exercise. It’s the key to making sharp, strategic decisions that drive real growth and guarantee your business is still around for the long haul.

The Three Pillars of Production Costs

To really get to grips with your costs, you need to break them down into three core components. Think of them as the pillars holding up your entire financial structure. Nailing each one is non-negotiable if you want a true picture of your company's health.

Here’s a quick summary to get you started:

The Three Pillars of Production Costs A quick summary of the essential components involved in calculating total production costs.

| Cost Component | Definition | Example (For a UK-based furniture maker) |

|---|---|---|

| Direct Materials | The raw ingredients that are physically part of the finished product. | The oak wood for a dining table, the screws holding it together, and the varnish for the finish. |

| Direct Labour | Wages and associated costs for the people directly making the product. | The salary of the carpenter who cuts and assembles the wood or the upholsterer who stitches the fabric for a chair. |

| Manufacturing Overheads | All indirect costs needed for production but not tied to a single item. | Rent for the workshop, electricity to run the saws, equipment depreciation, and the wages of the cleaning staff. |

Getting a clear handle on these expenses is the first step toward implementing effective high-impact cost reduction strategies that can seriously boost your margins.

By separating these costs, you gain a granular view of your spending. This clarity allows you to pinpoint inefficiencies, negotiate better prices with suppliers, and optimise your production workflow for maximum profitability.

Why This Calculation Is So Important

Knowing your cost per unit is absolutely crucial for setting the right price. If you price too low, you might not even cover your expenses, let alone turn a profit. Price too high, and you could be handing customers straight to your competitors.

These numbers are also vital for smart financial management. They feed directly into your operational budgets, giving you a firm grip on spending. For a deeper dive into this, our guide on budgeting and controlling has some really practical advice.

Ultimately, having accurate production cost data empowers you to make informed decisions—which products to promote, which to phase out, and where to invest your hard-earned money for future growth.

Getting to Grips with Direct Material Costs

First things first, let's talk materials. To figure out your production costs, you need to tally up every single raw material that physically goes into making your product. But it’s not as simple as glancing at the supplier’s invoice. That price is just the starting point.

To get this right, you have to calculate the true ‘landed cost’ of your materials. It’s a term for the total expense of getting something from the supplier to your workshop door. I’ve seen so many businesses trip up here, and it always leads to underestimating what things really cost.

Looking Beyond the Invoice Price

Think past what you paid the vendor. The real cost is a mix of other crucial, and often forgotten, expenses that can add up fast. A solid landed cost calculation always includes:

- Shipping and Freight: The charge to get goods from their warehouse to yours.

- Import Duties and Tariffs: The taxes you pay the government to bring materials into the UK. These can shift and really sting if you’re not prepared.

- Handling Fees: Charges for loading, unloading, and just moving your materials around at ports or warehouses.

- Insurance: Essential cover for your goods against damage or loss while they’re on the move.

Let’s run with an example. Imagine a small UK bakery ordering speciality flour from France. The invoice for the flour might be £500. But then they pay £50 for shipping, £25 in import duties, and another £10 for insurance. Suddenly, the true cost of that flour isn't £500; it’s actually £585. This is the number you need to be using.

How You Value Your Inventory

Once the materials are in your hands, the way you account for them can also sway your cost calculations and reported profits. The two go-to methods here are FIFO and Weighted Average. Which one you pick really matters, especially when material prices are all over the place.

- FIFO (First-In, First-Out): This method works on the assumption that the first materials you bought are the first ones you use. It's logical and usually matches how stock physically moves.

- Weighted Average Cost (WAC): This one involves calculating the average cost of all similar items you have in stock, then applying that average cost to each unit as you use it.

Back to our bakery. In January, they bought flour for £1 per kg. By February, the price had jumped to £1.20 per kg. If they use FIFO, the first loaf they bake in February uses the older, cheaper £1/kg flour. If they use WAC, they'd average the cost across both batches, meaning their material cost per loaf would be slightly higher right from the off.

Choosing a method isn't just a tick-box exercise for your accountant. It has a direct impact on your Cost of Goods Sold (COGS) and, by extension, your taxable profit.

When you nail down the full landed cost and make a conscious choice about your inventory valuation method, you stop guessing and start knowing your direct material expenses. That kind of accuracy is the bedrock of a solid pricing strategy and healthy profit margins.

Nailing Down Your True Direct Labour Costs

Once your materials are squared away, the next big piece of the puzzle is your direct labour cost. This is all about the wages for the people who are physically making your product—think of the editor cutting a film, the sound designer mixing audio, or the technician assembling a device.

It’s a common pitfall to only factor in the simple hourly wage, but that mistake can give you a dangerously inaccurate picture of your actual expenses.

To get your production costs right, you have to look beyond the payslip. The real cost of an employee is always significantly higher than their gross wage. It’s a bundled figure that includes all the mandatory on-costs that come with employing someone in the UK.

The Real Cost of an Employee

To get an accurate number, you need to add several crucial expenses into the mix. These aren't optional extras; they're fundamental parts of your total labour cost.

- Employer National Insurance Contributions: This is a significant percentage you pay on top of an employee's earnings.

- Pension Contributions: Your mandatory employer contributions to your team's pension schemes are a must.

- Holiday and Sick Pay: Paid time off is a cost that needs to be accrued and factored in from day one.

- Other Payroll Taxes: Don't forget any additional levies or taxes specific to your industry or region.

So, if you're paying an editor £20 per hour, the real cost might be closer to £25 per hour once you add these essential on-costs. Forgetting that extra £5 per hour across your whole team can completely wreck your project budgets and pricing strategy.

Your direct labour rate isn't just the wage you pay; it's the total cost to have that person working for one hour. Calculating this 'fully loaded' rate is the only way to ensure you're not underestimating one of your biggest production expenses.

From Hourly Rate to Project Cost

With your true hourly labour rate in hand, the next job is to track where that time is actually going. You need a reliable way to allocate labour hours to specific jobs, projects, or production runs. This is where meticulous time tracking becomes absolutely invaluable.

Modern software can make this process painless, letting employees log hours directly against the projects they’re working on. This data is pure gold for understanding which products are more labour-intensive and for managing variable costs like overtime, which can quickly spiral if left unchecked.

Smart time allocation is really a cornerstone of good resource management. For a deeper dive, check out our guide on what is resource planning.

Improving how you manage this process has a direct impact on efficiency. For UK manufacturers, labour productivity—the measure of output per hour worked—is a key metric. Between 1997 and 2007, this metric shot up by about 50%, a huge gain in efficiency. While that's a positive trend, the pressure is always on to manage labour costs effectively to stay competitive. You can explore more about UK production trends to see the bigger picture.

By calculating a fully loaded labour rate and diligently tracking time, you move from guesswork to precision. This accuracy stops you from underpricing your work and gives you the power to make smarter staffing and production decisions that actually protect your profit margins.

Mastering Your Manufacturing Overhead Costs

So far, we’ve nailed down the obvious costs—the raw materials you buy and the wages you pay. But what about everything else? All those background expenses that keep the lights on and the machines humming? These are your manufacturing overheads, the silent partners in your production costs.

Getting this part wrong is a fast track to misleading numbers and watching your profits mysteriously shrink. We’re talking about the indirect costs: factory rent, utility bills, equipment maintenance, even the salaries of your production supervisors. They are all absolutely essential, but you can’t tie them neatly to a single product. The real trick is to find a fair way to spread these costs across everything you make.

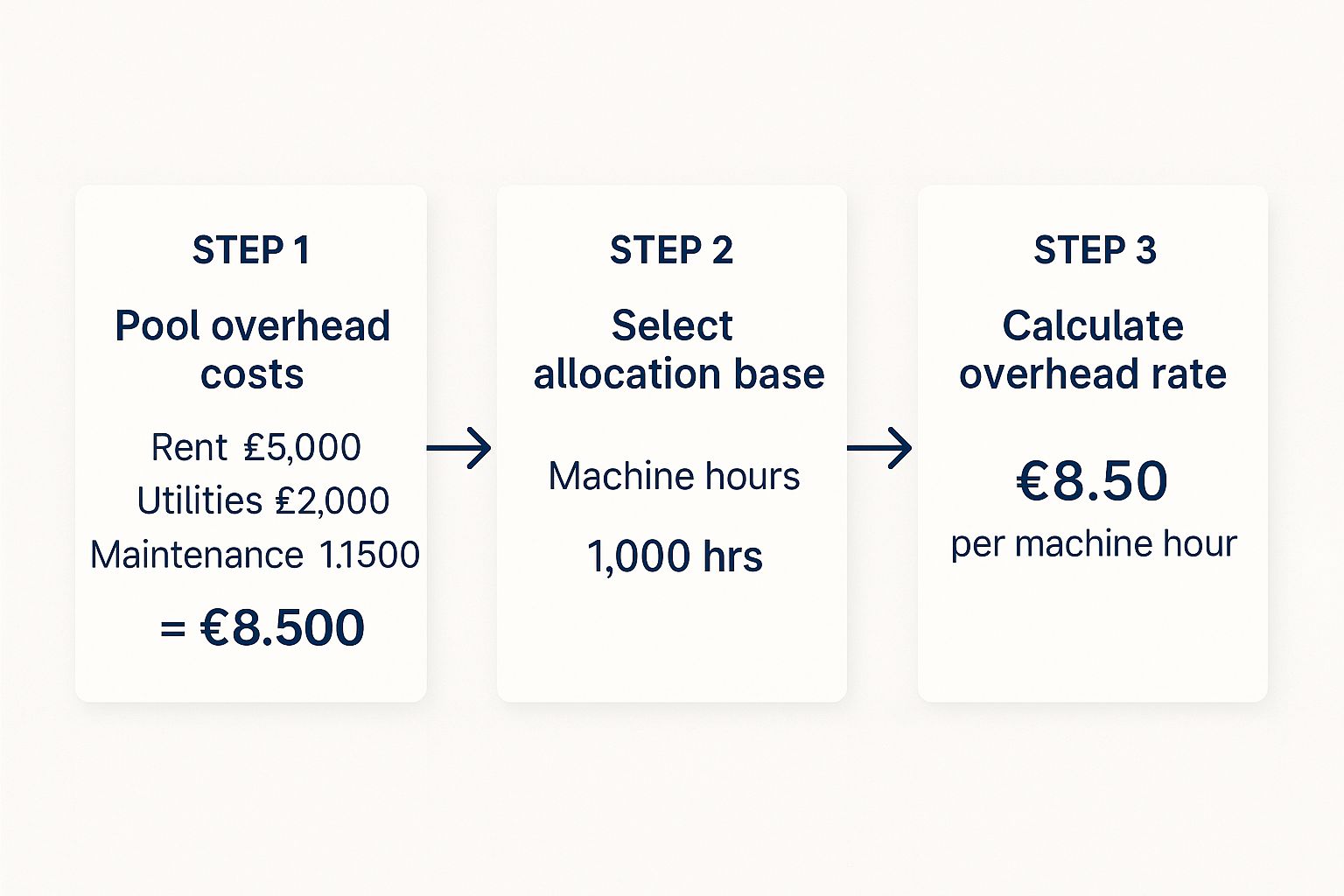

Pooling and Allocating Your Overheads

First things first, you need to gather all these indirect costs into one central 'pool'. Think of it as a bucket where you collect all your overhead expenses for a set period, usually a month. This gives you a single, clear figure to work with.

Once you have that total, you need a logical way to share it out among your products. This is where an allocation base comes in. It’s a measurable activity that’s closely linked to why you’re incurring these overheads in the first place.

Common allocation bases include:

- Direct Labour Hours: A solid choice if your production is very hands-on and labour-intensive.

- Machine Hours: The go-to option if your factory floor is buzzing with automated equipment.

- Units of Production: A simple method, but it really only works if you’re churning out a single, uniform product.

Choosing the right base is crucial. It’s what ensures each product carries its fair share of the factory’s running costs, giving you a much truer picture of its profitability.

The goal is to find a driver that best reflects how overhead resources are consumed. For a workshop making handcrafted furniture, labour hours just make sense. For a high-volume bottling plant, machine hours are a much better fit.

This simple infographic breaks down how to calculate your overhead rate.

As you can see, it’s about combining all those indirect costs and then dividing them by a relevant activity. The result is a simple, powerful rate you can apply across your production line.

A Practical Example in Action

Let's put this into practice. Imagine a UK-based clothing manufacturer. Last month, their factory overheads looked like this:

- Factory Rent: £5,000

- Utilities (Electricity & Water): £2,000

- Equipment Maintenance: £1,500

- Supervisor Salaries: £3,500

That gives them a total overhead cost pool of £12,000.

Since their operation is heavily automated with cutting-edge sewing and cutting machines, they’ve chosen machine hours as their allocation base. Over the month, their machines were running for a total of 2,000 hours.

Now for the easy part: Total Overhead Costs / Total Allocation Base = Overhead Rate £12,000 / 2,000 Machine Hours = £6.00 per machine hour

Suddenly, they have a powerful number. If a new batch of jackets takes 50 machine hours to produce, they know to allocate exactly £300 (£6 x 50) of overhead costs to that job.

Keeping a close eye on these costs is vital, especially when you consider the volatility in the UK manufacturing sector. During the pandemic, production plunged by a record 21.3% in April 2020, only to rocket back up by 41.4% a year later, highlighting just how quickly these costs can fluctuate. Discover more about these UK manufacturing trends and see why mastering overheads helps businesses navigate these economic swings.

Bringing It All Together: A Real-World Example

Theory is one thing, but let's get our hands dirty. Abstract numbers only get you so far; walking through a complete calculation from start to finish is what really makes the process click. We'll follow a fictional UK electronics company, "Echo Audio," as they pin down the production cost for their brand-new smart speaker.

Think of this as a repeatable blueprint. By seeing how Echo Audio does it, you'll get a feel for the logic and be able to apply the same steps to your own production line.

Identifying Direct Material Costs

First up, Echo Audio grabs their bill of materials for a single smart speaker. This is a simple list of every physical component that goes into the final product, along with its cost.

- Micro-processing Chip: £12.50

- Speaker Cone Assembly: £8.75

- Custom Moulded Casing: £6.20

- Wiring and Connectors: £2.15

- Packaging Materials: £1.40

Add it all up, and the total direct material cost per unit is £31.00. This is their baseline figure before a single person has touched it.

Calculating Direct Labour Costs

Next, they look at the human element. An assembly technician, earning a fully loaded rate of £24 per hour (this includes National Insurance and pension contributions), takes 30 minutes to assemble, test, and package one speaker.

The maths here is pretty straightforward:

£24 per hour / 2 (for 30 minutes) = £12.00 direct labour cost per unit.

Getting this number right is far more useful than a rough guess. It reflects the real cost of the skilled effort required for each speaker. It's a bit like creative work, where understanding the true cost of labour is everything—a principle that's also vital when budgeting for film production.

By breaking out and accurately costing their materials and labour, Echo Audio now has a clear view of their prime costs. This is the absolute minimum it costs to make one unit before any factory-wide expenses are layered on top.

Applying Manufacturing Overheads

Now for the tricky part: the factory's shared costs. Echo Audio's factory has total monthly overheads (think rent, utilities, supervisor salaries) of £40,000. They’ve decided that direct labour hours are the most sensible way to spread this cost across their products. Last month, their assembly team clocked a total of 2,000 direct labour hours.

This gives them an overhead rate:

£40,000 / 2,000 hours = £20.00 per direct labour hour.

Since each smart speaker needs 0.5 labour hours (30 minutes) to build, the overhead applied to each unit is:

£20.00 x 0.5 hours = £10.00 per unit.

To keep all these numbers straight, especially as your calculations get more complex, a good spreadsheet is your best friend. If you're new to spreadsheets, a solid Excel for Dummies guide can be a lifesaver.

The Final Calculation

With all three pieces of the puzzle in place, Echo Audio can finally calculate their total production cost.

Let's pull it all together in a clear table.

Sample Production Cost Calculation Per Unit A breakdown of the final per-unit cost for our example company, illustrating how each component contributes to the total.

| Cost Category | Calculation/Notes | Cost per Unit (£) |

|---|---|---|

| Direct Materials | Sum of all components in the bill of materials. | £31.00 |

| Direct Labour | 0.5 hours at a loaded rate of £24/hour. | £12.00 |

| Manufacturing Overheads | 0.5 labour hours at an overhead rate of £20/hour. | £10.00 |

| Total Production Cost | Sum of all costs. | £53.00 |

And there it is. Echo Audio now knows that each smart speaker costs exactly £53.00 to produce. This isn't just a number; it's the foundation for their pricing strategy, profitability analysis, and all future financial planning.

Still Have Questions About Production Costs?

Once you start getting into the nitty-gritty of the numbers, a few questions always seem to pop up. It's completely normal. We’ve pulled together some of the most common queries from UK business owners who are just getting their heads around how to calculate production costs.

Let's clear up those tricky spots so you can feel confident you're on the right track.

How Do I Handle Fluctuating Material Prices?

This is a classic headache for anyone making a physical product—the cost of your raw materials can swing wildly. The best way to manage this is to pick an inventory valuation method and stick with it. Consistency is key.

- First-In, First-Out (FIFO): This method assumes you use your oldest stock first. When prices are on the rise, this can work in your favour by matching your lower, older costs against current revenue.

- Weighted Average Cost (WAC): This approach smooths out the bumps by averaging the cost of all your available stock. It gives you a much more stable and predictable cost per unit over time.

Beyond accounting methods, it's always a good idea to regularly review your supplier contracts. See if you can negotiate bulk purchase discounts—locking in a good price can seriously buffer you against market volatility.

Don't let fluctuating costs derail your calculations. A consistent valuation method provides a stable baseline, turning unpredictable expenses into manageable data points for better forecasting and budget control.

Should I Include Non-Manufacturing Costs?

In a word, no. Keep them separate. The entire point of calculating production costs is to find the true cost of making your product. Things like marketing, sales commissions, or your office admin's salary are vital business expenses, but they aren’t part of production.

If you lump them in, you'll artificially inflate your cost per unit. That leads to wonky pricing decisions and a completely distorted view of how efficient your production process actually is. These costs are usually grouped as Selling, General & Administrative (SG&A) expenses and belong on their own line in your profit and loss statement.

What Is the Difference Between Prime Cost and Conversion Cost?

Getting your head around this distinction offers a much deeper insight into where your money is going. It's simpler than it sounds.

- Prime Cost: This is just the sum of your direct materials and direct labour. Think of it as the absolute core expense of creating a product.

- Conversion Cost: This is the total of your direct labour and manufacturing overheads. It’s the cost of converting those raw materials into a finished item.

You'll notice direct labour is the common thread, appearing in both calculations. These two metrics just give you different lenses to analyse your operational efficiency.

Ready to take control of your production budgets and scheduling? freispace offers the tools you need to manage resources, track costs, and streamline your entire post-production workflow. Discover a smarter way to manage your projects at https://freispace.com.